Turbulence outside: how outdoor industry players are struggling against market headwinds while others find pockets of profit

File photo by The Daily

Since the pandemic, the outdoor industry has faced significant headwinds, leading to widespread sales declines and operational challenges. Once buoyed by a surge in consumer participation, the market has since experienced a notable contraction, with over half of independent outdoor specialty retailers reporting decreases in sales in 2023.

In addition to decreasing demand, brands are grappling with supply chain disruptions, inflationary pressures, and evolving consumer preferences. These forces have squeezed profit margins, leaving even leading brands vulnerable.

To navigate these challenges, outdoor brands must employ strategic initiatives, such as strengthening brand loyalty, diversifying product offerings, and improving operational efficiency, in order to preserve margins and remain competitive in an increasingly difficult market.

Industry headwinds since 2020…

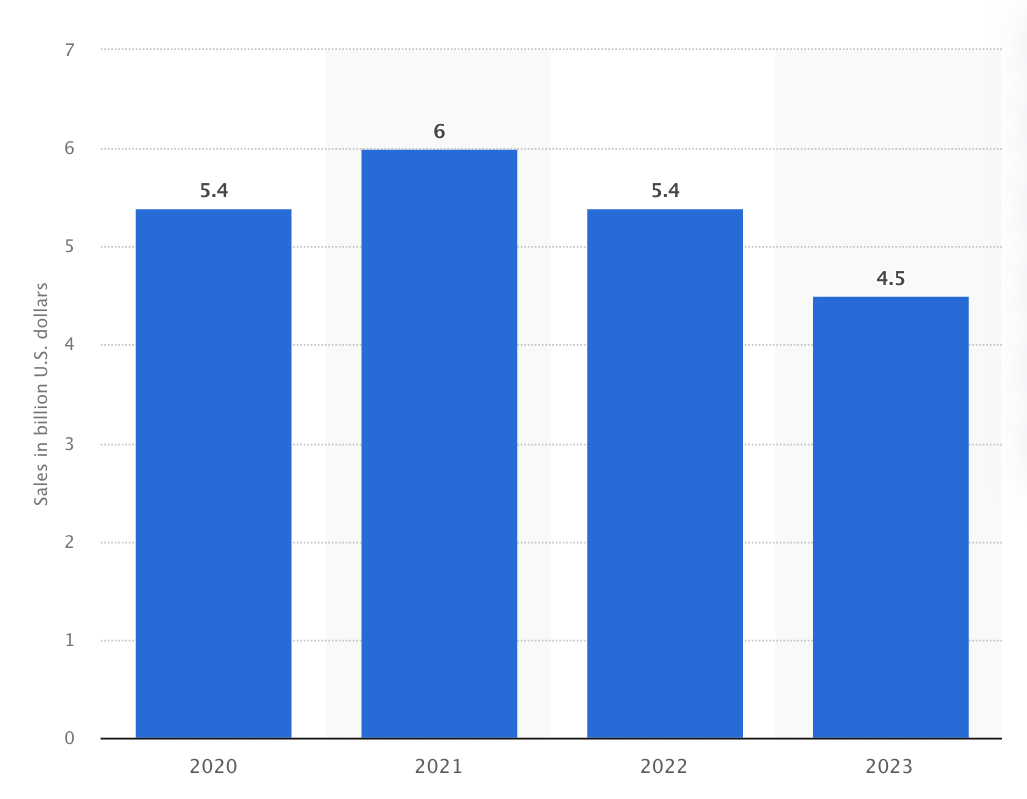

The outdoor industry has experienced notable declines in recent years, with 2023 proving especially challenging. More than half of independent outdoor specialty retailers reported sales declines of 10% or more, indicating widespread struggles throughout the sector. According to Kelly Davis, director of research at the Outdoor Industry Association, 2023 was "a really difficult year," with sales struggles seen across every retail channel.

This decline in sales coincided with a drop in consumer participation frequency, signaling a broader challenge for the industry. The pandemic had already hit the sector hard, as employment in outdoor recreation fell from 3.1 million in 2019 to 2.77 million by 2021—a more than 10% decrease. While some categories managed to stabilize after the initial COVID shock, 2023 saw significant dips in key product areas. Apparel, which represents over half of the industry’s sales volume, was down by 3%, while equipment sales dropped by 3.4%. The decline was also evident in unit sales, with apparel sales falling 6.1%, equipment sales down 5%, and footwear taking the hardest hit, down 10%.

The combination of these factors paints a grim picture for the outdoor industry, which is grappling with both lower consumer demand and operational difficulties in the post-pandemic landscape.

What is causing the downward trend?

The outdoor industry's recent struggles have been driven by a combination of post-pandemic market volatility, inflationary pressures, supply chain challenges, evolving consumer preferences, and profit pressures. Consumer demand has become increasingly unpredictable, with spending fluctuating month to month. In August 2023, personal consumption expenditures on sporting equipment, supplies, guns, and ammunition fell by 0.9% compared to the previous month, only to rebound by 0.7% in September. This volatility has made it difficult for retailers to accurately forecast demand and maintain consistent sales.

The industry is also experiencing a contraction from the pandemic-era surge in outdoor activities, as the market adjusts from the "Covid bubble" of heightened demand. This "right-sizing" is creating new challenges in 2023, and the effects are expected to continue into 2024. One significant consequence of this contraction has been excess inventory, which has led to a promotional environment that is cutting into retailers' profit margins. Additionally, inflation and broader economic uncertainty have affected consumer spending habits. Although fears of a recession loom, the resilience of U.S. consumers has somewhat mitigated these concerns.

Suppy chain disruptions

At the same time, supply chain disruptions, while not as prominent as they were during the height of the pandemic, remain a challenge for the industry. Supply chain disruptions have played a significant role in the challenges faced by the outdoor industry, affecting everything from product availability to production timelines. For instance, many brands struggled to secure essential materials during the height of the pandemic, particularly those relying on international suppliers. Patagonia, known for its sustainable outdoor gear, faced production delays in 2021 and 2022 due to shortages of recycled materials and labor disruptions at key manufacturing sites. Similarly, REI experienced delays in receiving essential outdoor equipment such as tents and bicycles, forcing the company to adjust its inventory planning and customer communication strategies.

These supply chain problems have not fully abated. In 2023, fluctuating availability of raw materials and continued port congestion led to longer lead times for some outdoor products, particularly those with complex manufacturing processes. The ripple effects of these delays have been felt across the industry, contributing to a buildup of excess inventory at times when demand was lower than anticipated, further compounding the promotional environment that is hurting retailer margins.

Evolving consumer preferences

Meanwhile, evolving consumer preferences are pushing brands to rethink their product strategies. Consumers are now prioritizing versatility and durability in their outdoor gear, seeking products that balance performance with longevity. This shift requires companies to adapt not only their offerings but also their marketing strategies to meet changing demands. Recent research suggests that “non-traditional” outdoor brands like Vuori, Hoka, and On are outperforming their contemporaries at retail stores across the country. This is largely due to a shift in the outdoor consumer landscape toward product characteristics that align with a generally active lifestyle and away from technical product specifications that align with outdoor performance.

Large incumbents vs. pure-play e-commerce brands

Finally, pure-play e-commerce outdoor brands are facing the same pressures that other DTC shops are tackling: the dominance of three powerful oligopolies that have eroded profit margins. First, the customer acquisition oligopoly of Google, Meta, and Amazon now commands 15-40% of online revenue, where brands once relied on free organic content. Second, the product fulfillment oligopoly, led by UPS, FedEx, and Amazon, has consistently raised rates by about 6% annually, capturing 15-20% of online revenue. Lastly, the payment processing oligopoly of Visa, Mastercard, and Amex still claims 3-3.5% of revenue, despite advances in technology. This squeeze on margins has left even well-funded DTC brands like Allbirds, who has attempted to break into outdoor-adjacent markets with its running shoes, struggling to achieve profitability.

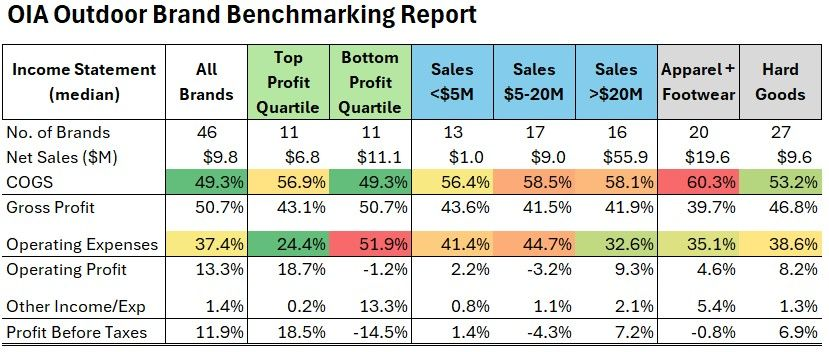

The following chart displays profitability benchmarks for outdoor players. One major callout is the stark ~52% for operating expenses within the Bottom Profit Quartile.

This is likely in part due to those brands’ have less developed wholesale channels and spending more money on Google and Meta advertising to drive demand.

What can outdoor brands do to weather the storm?

Based on our research, outdoor brands must consider the following strategies selectively in order to navigate the current industry headwinds and mitigate risk:

- Strengthen brand loyalty by investing in brand-building and maintaining a premium image

- Diversify product assortment to expand beyond core offerings to cater to a broader range of outdoor enthusiasts

- Innovate product offerings with technology and sustainability

- Balance channel strategy—leveraging traditional retail, e-commerce, and direct-to-consumer (DTC) models—to reach consumers more effectively

- Drive operational efficiency through supply chain management and cost control (e.g., marketing and advertising)

Below are a few examples of outdoor or outdoor-adjacent brands that have successfully employed some or all of these strategies to outperform the rest of the market in recent years:

On Running:

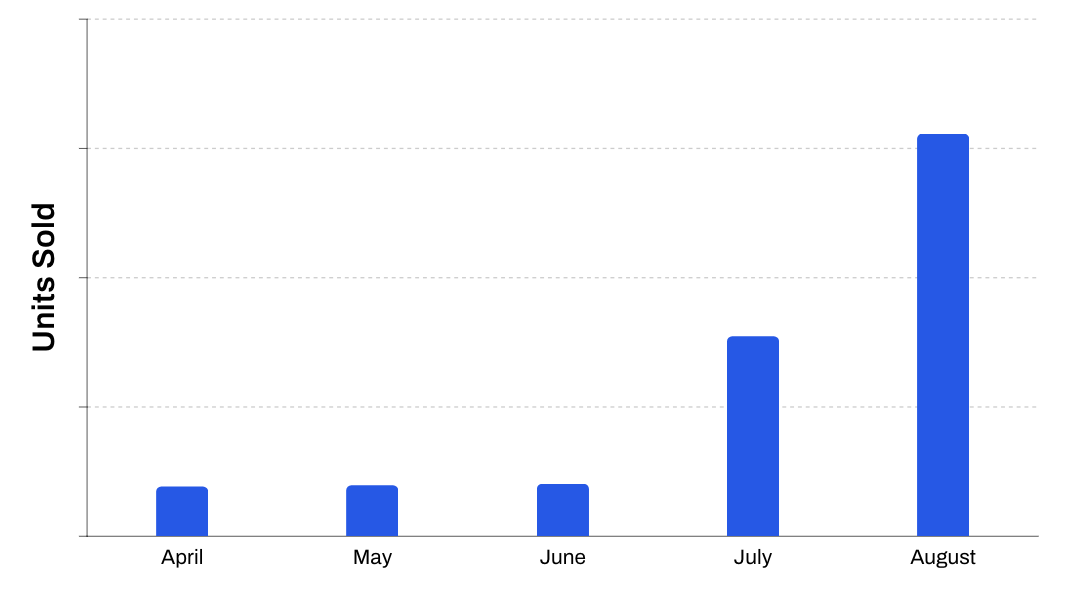

On Running’s innovative cloud-cushioning technology – which was revamped to be “softer” in recent years, appealing to the US market – and expansion into apparel have fueled its growth. By balancing e-commerce and DTC sales channels, the brand has outpaced competitors and posted strong numbers despite industry challenges. On Running’s online sales have grown over 500% since the start of Q2, according to Particl-tracked inventory.

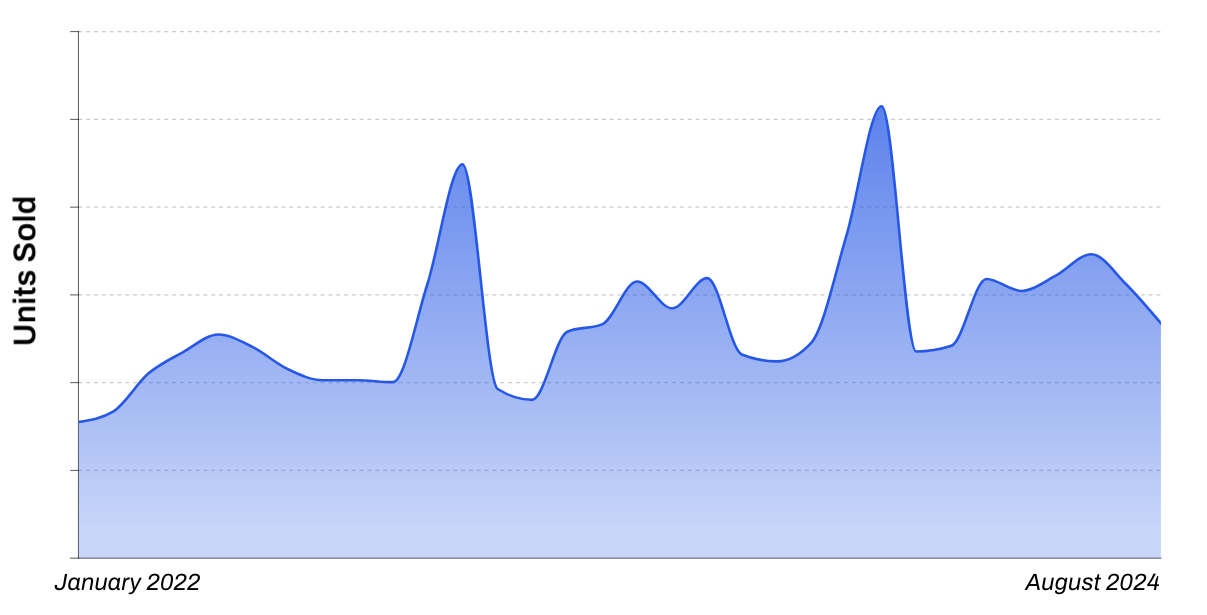

Yeti Australia:

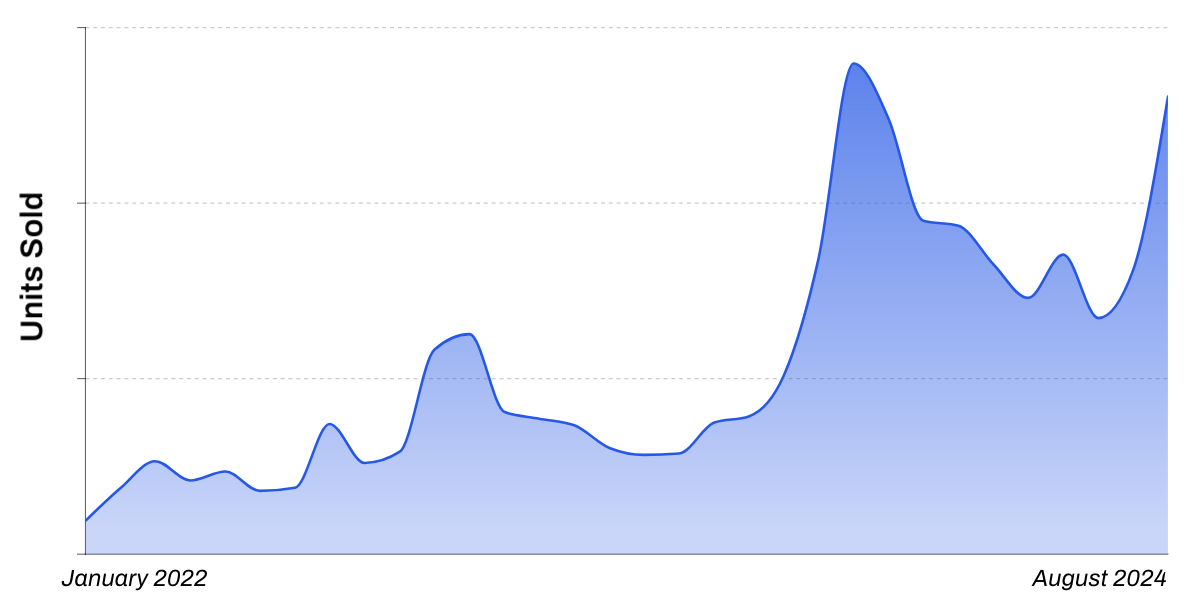

Yeti's premium image and product diversification into bags and outdoor gear have strengthened its position. A strategic mix of DTC, e-commerce, and retail channels has helped Yeti continue growing in a tough market. International expansion has also been a successful strategic play, as units sold have grown tremendously (over 1000%) since January of 2022.

Vuori:

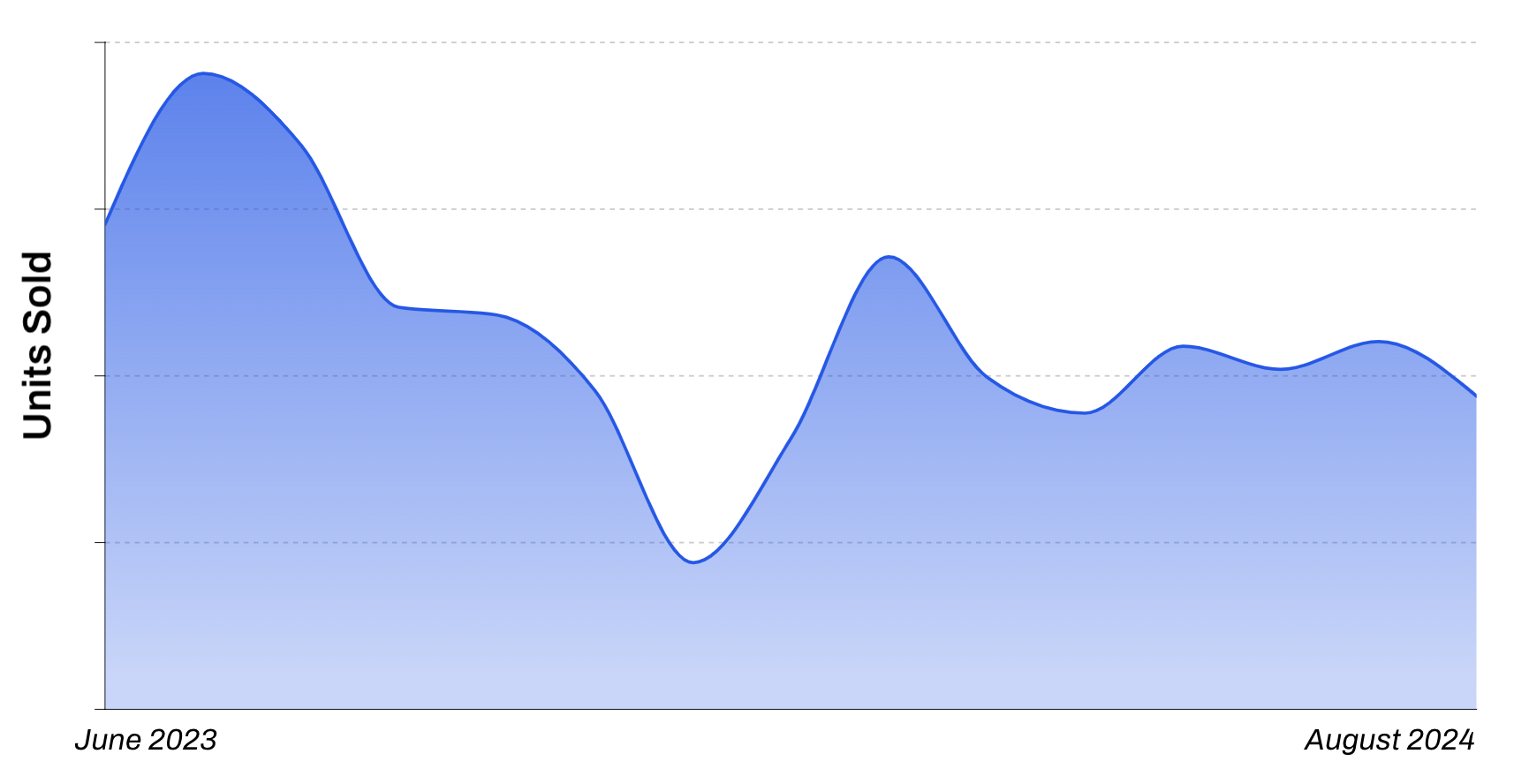

Vuori’s focus on sustainability and versatile activewear has driven its success. By balancing DTC, e-commerce, and retail, and capitalizing on the athleisure trend, Vuori has maintained strong growth amidst market declines. Many outdoor and sports retailers have noted how much share Vuori has captured in their stores, including spend from traditional “outdoor enthusiasts” who are looking to purchase products that can address multiple activities. Vuori has posted consistent online growth YoY since the end of 2021 (below).

Sources:

OIA Report

Colorado Sun

Outdoor Employment

Statista

Capstone Partners

Capstone M&A

SGB Media

Camoin Associates

Outsize Consulting